For my own accountability and clarity of thinking, I am writing this quickly on the night of March 16, 2020. The S&P closed at 2,386, down 12% on the day.

Somehow, someway I am bullish on the market at these levels with a bias towards aggressive positioning on incremental investments from here.

I have zero idea if this a bottom. Zero idea.

That said, here are some very recent views I that have helped me arrive at a constructive outlook:

And generally this entire thread from WexBoy:

While I am mixed on whether these specific China COVID-19 read-throughs are right (said another way, “I HAVE NO IDEA ABOUT VIRUSES“), the graphics alone are worth highlighting:

As an aside, I have gotten a tremendous amount of value out of FinTwit the last few years. Thank you all.

I keep a curated list of ~100 accounts here that I encourage you to follow.

THE THESIS

So the themes of my upside thesis:

- Upward margin reset – a partial replay of the long term overall corporate profit margin reset coming out of 2008. Even a short downturn will show S&P500 sized companies where they can get by with less (or more automation) and also as a HR “kitchen sink” for clearing out the bottom of the employee base.

- TINA (“There is No Alternative”) and low rates. If I had to guess, I will err on the side of global rates remaining lowish. Rates can be a good bit higher than today’s and still offer equity support and an upward P/E re-rating.

- Little long-term demand destruction. There are few sectors I see COVID-19 materially changing long-term demand. When I was diligencing short positions on the cruise lines (RCL, CCL, NCLH) a week ago (feels like an eternity), I visited Reddit’s r/cruising subreddit. While there is a selection bias toward dies hard cruise fanatics there, I was shocked by the number of comments where a modest discount would get these people to book a cruise now! In a “LOL, Nothing Matters” world, enough people are not going to change their behavior 12 months from now because of COVID-19.

- Size and speed of stimulus relative to an economy that has been pretty good on an LTM basis. If we truly adapt massive stimulus consistent with a war-time mentality (see Olivier Blanchard above) combined with an aggressive Fed, the rebound could be quite strong. And a thank you to Andrew Yang for moving the Overton Window towards direct cash transfers.

- Good black swan -> something goes right. Not counting on it….but a novel treatment or vaccine….or something unexpected goes right.

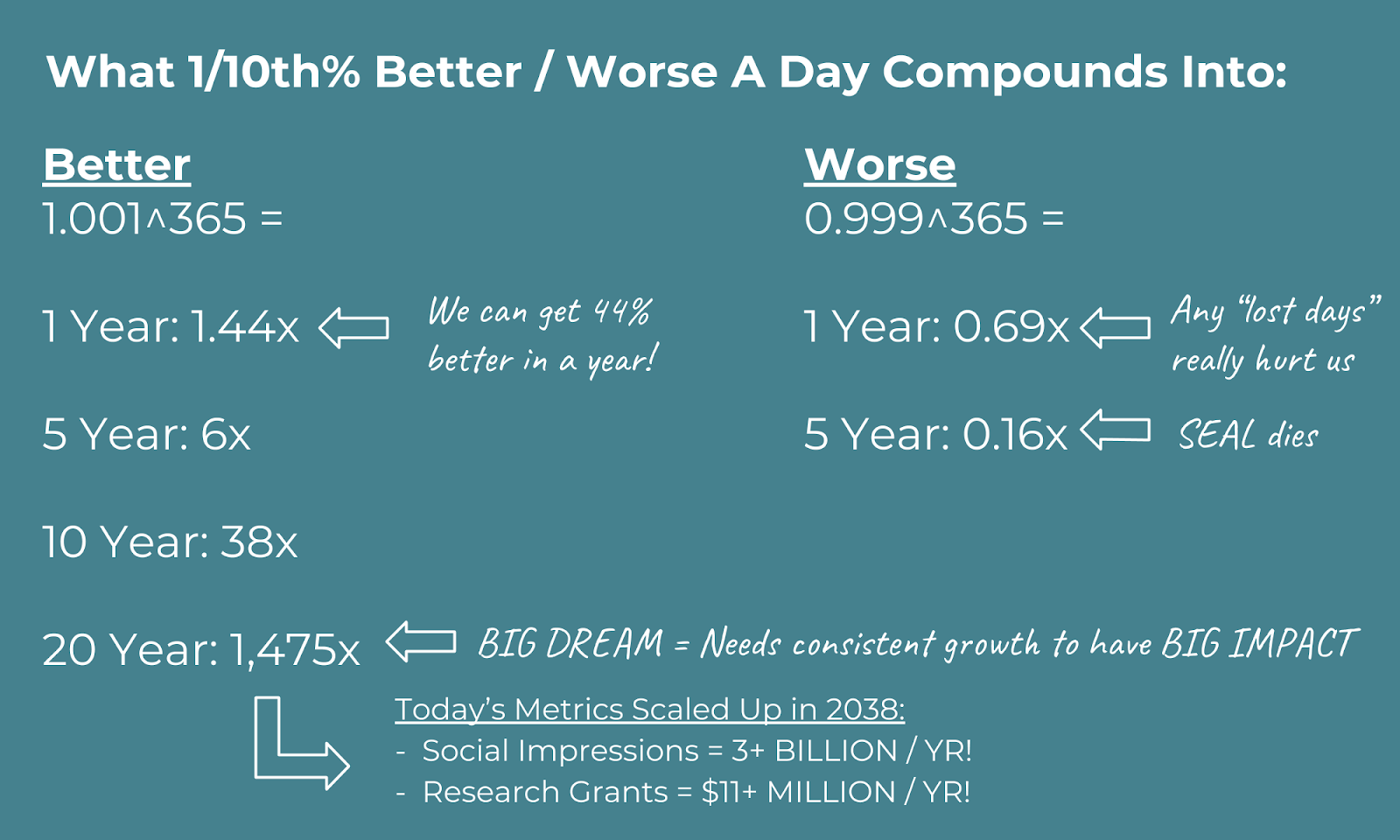

Where do I think this thesis adds up to? A melt-up market, yielding an S&P500 of ~3,500 to ~4,000 within 36 months.

I think that risk-reward is interesting but not phenomenal.

This post will probably get push back along the lines of “SPX 3,500 is not worth the chance we go down to [INSERT VARIOUS BOTTOM PREDICTIONS HERE].”

And that is entirely fair. We likely will go lower from SPX 2,400! And I hope to keep adding to these names down there if needed.

SOME RISKS

A non-exhaustive list of what could go wrong:

- Bad print after bad print. Q2 GDP comes in 11% down, not 5% down. Shockingly low PMI readings. And so on. Investors capitulate, multiples contract.

- COVID-19 lockdown lasts into August or September.

- Socially unpalatable financial institution failure. More specifically, an international bank (strictly theoretically, Deutsche Bank) and/or large “hedge fund” (strictly theoretically, Citadel or Bridgewater) collapses where coordinating a rescue would be so socially and politically toxic to be unworkable.

- Prominent growth story blows up. I have real concerns about the market reaction in the event of Tesla collapse.

- COVID returns in the fall or flares up in other regions.

- Acts of war break out

- Accounting frauds revealed – further contributes to multiple contraction

- Significant natural disaster

- US political gridlock prevents sufficient stimulus

MY POSITIONS

Long-term holdings I am comfortable adding to incrementally at these levels:

- Sharpspring (SHSP)

- Xero (XRO / XROLF)

- New Relic (NEWR)

- Floor & Decor (FND)

- TPI Composites (TPIC)

- RCM (RCM)

- Envestnet (ENV)

- LiveChat (LVC on Polish Exchange)

Speculative “aggressive basket” names I am buying (with an important preface that many of these are low conviction

- TripAdvisor (TRIP) and Liberty TripAdvisor (LTRPA)

- Millicom (TIGO)

- Anheuser-Busch (BUD)

- US Foods (USFD) (warning: probably too early here)

- Sky Champion (SKY) (via @RandolphDuke7 (fka @ValueTrap) flagging during 2018 downturn)

- Aspen Group (ASPU)

- Trex (TREX) (via @EddyElfenbein)

- Re/Max (RMAX) (via good Value Investor Club idea)

- WestRock (another good Value Investor Club idea)

- Sensata (ST)

- Home Depot Supply (HDS)

- Beacon Roofing (BECN)

- Jeld-Wen (JELD)

- Douglas Dynamics (PLOW)

- Recro Pharma REPH (via a good Value Investor Club write-up and some fund letter on Seeking Alpha)

- Wells Fargo (WFC)

- Ulta Beauty (ULTA)

- Names next on the watchlist (no positions yet):

- Univar (UNVR)

- Endurance International (EIGI)

SaaS names I am adding to :

- ZenDesk (ZEN)

- Medallia (MDLA)

- PagerDuty (PD)

- BlackLine (BL)

- SurveyMonkey (SVMK)

- Sprout Social (SPT)

- Alteryx (AYX)

- Speculative name on near-term watch list

- Nitro Software – recent small cap IPO in Australia – thesis as cheap PDF and e-signature software that enables “digital transformation” for more price-sensitive enterprises. Morgan Stanley underwrote IPO and has coverage.

Longer-term holdings I probably will just hold with low conviction (and I take into account my low-basis in certain of these that might otherwise change my view):

- Brookfield Renewable (BEP)

- Match Group (MTCH)

- Air Products (APD)

- LiveRamp (RAMP)

- LGI Homes (LGIH)

And in full transparency, here are some regrettable holdings that I have no idea what to do with:

- Burford Capital (BUR) – key lesson learned: don’t piggyback write-ups. I was told this is the Blackstone of litigation finance. Ugh.

- PAR Technology (PAR) – again, following a write-up and I don’t know the underlying details well enough. Ugh. Probably good upside from here though.

- Zuora (ZUO) – a pre-IPO investment. No idea if the public markets will ever like them.

- Elastic (ESTC) – another following other investors mistake. Maybe good upside from here, maybe not.

- Nutanix (NTNX) and TeraData (TDC) – Ugh. Not a good time for re-rating stories.

To quote @NonGaap, I might have to go “Donner Party” on these regrettable holdings.

Final disclosures: I have smallish and pre-existing short positions on:

- Tesla (TSLA)

- Royal Caribbean (RCL) – thank you @Keubiko!

- Country ETFs (Canada – EWC, Australia – EWA, and India – INDA)

Good luck to all.

Image Credit: Photo by NOAA on Unsplash. My rationale: captures “Snow in the Desert” – I experienced desert snow for the first time this fall on a trail run in Red Rock Canyon. I can’t quite articulate it, but that temporary and strange set-up reminds me of today. Memorable no matter what happens from here.